A Theory of Corporate Joint Ventures

In a corporate joint venture, two corporations—often competitors—collaborate on a project. But how can corporations be partners and competitors at the same time? Though it sounds like a contradiction, such collaborations are commonplace. Many of the most familiar products come from corporate joint ventures, from high-technology like solid-state drives for laptops or rocket boosters for NASA’s Discovery program, to everyday items like Star Wars action figures and even Shredded Wheat cereal. Indeed, Meinhard v. Salmon, arguably the most celebrated case in all of business law, arose out of a dispute within a joint venture. Yet unlike more familiar business forms such as corporations or LLCs, neither case law nor statute provides a clear statement of what a joint venture is or even which laws apply. Given this confusion, it is not surprising that the literature has not produced a unified theory of the corporate joint venture: a coherent statement of both what it is as a matter of law and how it functions.

This Article offers a theory of the corporate joint venture. It traces the development of joint venture law and practice from its origins in 19th-century American case law to the present. The central claim is that at the heart of joint venture law and practice, there is a singular legal problem: the foundational fiduciary duty that applies to all business forms—the duty of loyalty—is inherently contradictory within the context of a joint venture. The contradiction arises because the law has effectively treated joint ventures as partnerships whose members happen to be corporations. This formulation is contradictory because partnership law requires each corporation to be loyal to the other, while corporate law requires each agent to be loyal only to her own corporation. Thus, joint venture law both requires and prohibits a division of loyalty.

The Article first shows how this inherent conflict was a latent motivation behind the path of early case law, as well as how case law subsequently obfuscated the conflict and left a legacy of confusion. It then uses economic theories of business organization and contract law to explain how the joint venture forms we observe today resolve this conflict through a hybrid corporate-contract form. Finally, it demonstrates empirically how the modern contractual solution has engendered a new set of fiduciary problems via networks of joint venture connections across corporations in an industry. The Article concludes by offering policy prescriptions to tackle these problems and clarify the law of joint ventures.

Table of Contents Show

Introduction

A little loyalty is a dangerous thing.[2] In many spheres of life—love, war, family, friendship—divided or conditional loyalty is no loyalty at all. The same applies to the law. Law requires loyalty whenever it finds a relationship exhibiting two elements: agency and trust. Both are essential. Agency is the legal authority of one person (the agent) to make decisions on behalf of another (the principal).[3] Trust is the principal’s belief that the agent will act in her interest, even when the agent’s behavior cannot be observed or verified in court. More agency requires more trust, while greater trust supports greater agency. When these two elements extend together, the law recognizes the relationship as fiduciary.

Fiduciary law takes as its point of departure the idea that the agent’s loyalty is undivided. An agent must act in the best interest of the principal. Departures from this ideal inspire vast literatures that study “agency costs,” the catchall to describe any deviation from a first-best, efficient outcome that arises from this principal-agent relation.

Agency costs abound in both corporations and partnerships. We find them in corporations because shareholders’ and managers’ incentives are misaligned. We find them in partnerships because partners exercise mutual agency vis-a-vis each other and often disagree over what constitutes the partnership’s “best interest.” The law thus demands loyalty from agents of both. Corporate agents owe a duty of loyalty to the corporation; partners owe a duty of loyalty to each other.[4]

What about the case in which two corporations form a partnership? This is the case of joint venture. Corporations might form a joint venture because they desire something more collaborative than arms-length contracting but less permanent than merger. Though joint ventures can arise among both natural and legal persons, my focus here is on joint ventures between corporations.

Corporate joint ventures stack the agency costs of corporation and partnership on top of each other. The result is a seemingly contradictory relation: how can corporations be partners and competitors at the same time? At first blush, they cannot. “Competing with your partner” is anathema to partnership law. The partnership duty of loyalty requires each partner “to refrain from competing with the partnership in the conduct of the partnership business.”[5] This applies with full force to joint ventures. In the enduring words of Judge Cardozo, the standard of behavior among co-venturers is “[n]ot honesty alone, but the punctilio of an honor the most sensitive.”[6] Between co-venturers, “the rule of undivided loyalty is relentless and supreme.”[7]

Yet undivided loyalty is hardly “relentless and supreme” in modern joint ventures. We regularly observe joint ventures in which corporate co-venturers continue to compete against each other. Such joint ventures are found within many industries—aerospace, telecom, integrated circuits, food and beverage, retail investment, heavy industry, and pharmaceuticals.[8] The modern joint venture thus begins with precisely the opposite presumption: the duty of loyalty is necessarily divided between competing partners. This division will produce its own unique kind of agency cost—a fiduciary conflict that is inherent in the structure of joint ventures.

This Article argues that the intrinsic fiduciary conflict is the fundamental legal challenge facing corporate joint ventures. It demonstrates how the law and private parties can and should respond to this challenge. The argument proceeds in three parts. First, I show that the fiduciary duties of corporate joint ventures are contradictory. The literature has overlooked this contradiction, even though it is the fundamental legal problem for joint ventures. The problem is that both corporate law and partnership law apply to joint ventures. The contradiction is that corporate law imposes a duty of undivided loyalty to one’s own company, while partnership law imposes the same duty to one’s partner company.

I begin by showing that this conflict was a latent motivation behind the evolution of joint venture case law, from its origins in the nineteenth century to the present. I then argue that modern corporations resolve this conflict through a hybrid contract-entity form in which they (1) alter the loyalty duties through a covenant not to compete (CNC) and (2) avoid conflicts by operating the venture through a separate entity. This theory thus offers a new explanation behind CNCs: in corporate joint ventures, a CNC establishes coherent fiduciary duties.[9] It also demonstrates a counterintuitive purpose for the creation of a separate entity: though a separate entity is often thought to create conflicts by introducing the principal-agent problem, corporate partners use a separate entity to avoid conflicts by delegating decisions for which the corporate partners are conflicted.

This Article builds on a literature that seeks to identify the key legal features that distinguish the law of contract from the law of business entities. Prior literature has highlighted a functional distinction: the law of business entities enables investors to create a legal person—a corporation, LLC, or other entity—with power to own and dispose of property. This in turn enables investors to cleanly separate business assets from personal assets.[10] The resulting “asset partition” would be infeasible through contract law, which contains no such power to create legal persons.

Here I introduce a complementary and counterintuitive role for entities. When the investors themselves have conflicting objectives, how can they realize gains from collaboration? The solution is to collectively delegate decisions to an “agent”—i.e., a separate legal entity. Crucially, this entity is populated with (natural) persons who owe no duties to the investors directly; rather, their duties are owed to the entity itself. Their objective is to maximize the joint interests of the conflict-ridden principals. I use a case study to demonstrate how this works in practice.

The Article then investigates whether and how the law enables investors to enforce this structure. States vary considerably in the extent to which they are willing to enforce CNCs. Although the literature has acknowledged this variation across states, it has not previously considered the consequences of this variation for corporate joint ventures. Corporate co-venturers would encounter serious problems if they sought to enforce their fiduciary obligations in places like California, which heavily restricts both the alteration of fiduciary duties and the enforcement of CNCs.

For this reason, the Article recommends the creation of an “internal affairs” doctrine for corporate joint ventures. Under this rule, parties would be allowed to choose the law that governs their joint venture, and courts would honor that choice even if it meant enforcing a CNC. Courts should be more willing to enforce CNCs in corporate joint ventures (especially ones that have already passed federal antitrust scrutiny) because the usual policy arguments against them do not apply. Enforcing these provisions would generally not restrict the mobility of employees at either firm. Rather, they would only prevent the corporate partners themselves from opportunistically poaching the venture’s business opportunities. Voiding such agreements would thus deter collaborative innovation while yielding relatively few competitive benefits.

Finally, the Article documents the existence of joint venture networks, in which corporations in the same industry maintain multiple partnerships with overlapping membership. These networks compound the relatively simple fiduciary conflicts that obtain in isolation. They also reveal the robustness of the structure of modern corporate joint ventures, particularly its ability to compartmentalize fiduciary conflicts that might otherwise propagate over the joint venture network. I conclude by considering the implications of these networks for the theory of the firm, which canonically treats firms as distinct, nonoverlapping units of production.[11]

The rest of this Article is organized as follows. Part I examines the law and origins of joint venture and its intrinsic fiduciary conflict. Part II uses a case study from the aerospace industry to analyze how corporations respond to the intrinsic fiduciary conflict of joint venture. Part III discusses enforcement of joint venture agreements and the Article’s recommendation for an internal affairs doctrine. Finally, Part IV demonstrates how the hybrid corporate-contract structure of modern joint ventures sustains joint venture networks; it also discusses implications for the theory of the firm.

I. The Intrinsic Fiduciary Conflict of Joint Venture

Though largely forgotten, the law of joint venture originated as a direct judicial response to the intrinsic fiduciary conflict. In this Section, I set forth three stages in the development of this law. The first was outright prohibition: corporations were not permitted to participate in any partnership. The second was a short-lived exception to this rule—the doctrine of “joint venture,” which permitted corporate partnerships so long as they were limited in scope. In the third and final stage, states overruled the prohibition by statute. I conclude that the arc of joint venture law was not toward “solving” the intrinsic fiduciary conflict, but instead toward relinquishing the problem-solving onus onto private parties.

A. Legal Origins

1. The Rule Against Corporate Partnerships

Nineteenth-century American corporations were prohibited from participating in any partnership, be it with another corporation, an individual, or any other legal person.[12] The few exceptions to this rule were so limited and distinguishable that they seem to prove the rule. For example, courts occasionally granted exceptions based on theories of unjust enrichment. A typical case involved a corporation that benefited from an ultra vires partnership association.[13] In these cases, the partnership was recognized only as a means to calculate the appropriate disgorgement remedy; the partnership itself was not permitted to continue operations.[14] Even in such cases, however, courts did not always grant the exception.[15]

There were two reasons why courts prohibited corporations from forming partnerships: the ultra vires doctrine and the contradiction between partnership and corporate law duties. The first reason came from the historical state monopoly on incorporation. Before states adopted general incorporation laws, only acts of the legislature granted corporate charters, and charters were therefore public law.[16] Courts recognized only two types of limited powers that the legislature could confer through a charter: (1) express powers that were granted in the charter, and (2) implied powers that were “necessary and proper” to exercise express powers.[17] Any corporate act that did not rely on one of these two powers was prohibited under the ultra vires doctrine.

Charters did not typically include an express power to form partnerships, and courts would not infer an implied power. There were several reasons. The most important was that, by forming a partnership, two corporations could effectively merge, thereby forming a “new” corporation. Since only the legislature could grant incorporation status, this was ultra vires.[18] Though the ultra vires doctrine was the main basis for prohibiting corporate partnerships, a few courts offered a second.

The second reason why corporations could not form partnerships was because the joint application of corporate law and partnership law produced an inherent fiduciary conflict. The influential case of Whittenton Mills v. Upton is an early example of how the law grappled with this fiduciary tension.[19] The Whittenton Mills corporation, a Massachusetts cotton manufacturer, had entered into a partnership agreement with William Mason, a natural person. Mason was to provide manufacturing equipment and would share in Whittenton Mills’ profits. All went well until Mason suddenly declared bankruptcy. In the insolvency proceedings, Mason’s creditors brought an action to collect against Whittenton Mills as Mason’s general partner. The collection procedure would have liquidated the corporation, but the court held that Whittenton Mills did not have the capacity to form a partnership. The insolvency proceedings against Whittenton Mills were vacated.[20]

The court reasoned that Whittenton Mills’ charter could not have conferred an implied power to form partnerships because Massachusetts business law and policy relied on the corporation’s capacity “to manage its affairs separately and exclusively.”[21] The power to form partnerships would have contradicted this policy because it would have enabled the corporation’s fiduciaries—its directors and officers—to delegate decision-making authority to the other party in the partnership. Of course, much of a manager’s job is in delegating both tasks and authority. But a partnership contemplates a total and irrevocable delegation: as the corporation’s general partner, Mason would have had authority equal to that of the corporation’s directors, officers, and shareholders combined.[22] The effective authority would have been even greater since Mason could have acted as an individual, rather than through the checks and balances of corporate command. Indeed, had the partnership been recognized, Mason’s unilateral decisions would have liquidated the corporation.[23]

2. The Exception for “Joint Venture”

Like any bright-line rule, the problem with the prohibition of corporate partnerships was its overinclusiveness. The rule was based on the worst-case scenario of general partnership, cases like Whittenton Mills, in which one person could claim total authority over the corporation. But not every corporation that sought a partnership-like relationship wanted to form a general partnership. The purpose of a corporate partnership was not to delegate authority per se and certainly not to authorize would-be partners to dispose of corporate property without limit. Instead, the purpose was to engage in a limited sphere of cooperation with an entity outside the corporation—or, to use the Coasean lingo, to coordinate with another firm without the price mechanism. These corporations therefore sought a relation that was fiduciary in nature: something less formal than partnership yet stronger than contract.

Joint venture was the judicial response to this demand. Joint venture law was created as an exception to the general rule against corporate partnerships. Courts justified the joint venture exception by deemphasizing its partnership-like qualities while emphasizing its circumscribed, contractual nature.

The key judicial move was to separate the two components of partnership: co-ownership of assets and mutual agency. Agency, the more problematic of the two, was tamed by emphasizing the joint venture’s limited business scope.[24] So long as the corporation’s co-venturer did not exert “too much” control, courts reasoned that the business deal simply did not implicate partnership law. It may have looked and quacked like a partnership, but its “limited purpose” was sufficient grounds for concluding otherwise.

After courts dispatched the agency problem, all that remained was co-ownership. The case for corporate co-ownership was easy. Common law had long held that co-ownership, by itself, was not sufficient to form a partnership.[25] And since corporate charters already included an express power of individual ownership, courts could reason by extension that co-ownership was an implied power, “not inconsistent” with a charter that was silent on the issue.[26]

As a legal doctrine, however, joint venture did not last long. By the mid-twentieth century, courts openly acknowledged that the joint venture exception had effectively swallowed the rule.[27] Joint venture law was closer to a sub silentio overruling than a carefully crafted carve-out.[28] One scholar of the time wrote that it “indirectly give[s] the corporation the implied power to enter into a partnership agreement,” and further that a hypothetical law expressly granting the same power “would do nothing more than recogniz[e] an accomplished fact.”[29]

3. Statutory Authority for Joint Venture

Over the next few years, all state legislatures eventually passed such laws, expressly granting corporations power to form partnerships. These laws overruled both the prohibition of corporate partnerships and the ultra vires doctrine by essentially flipping the default authority: previously, the ultra vires doctrine required every corporate act to be authorized by an express (or implied) charter provision. Now, so long as the charter does not expressly provide otherwise, corporations have authority to carry out any lawful act. This includes the authority to engage in any business or business form.[30] A corporation can form partnerships[31] (and vice versa),[32] convert into a partnership,[33] merge with a partnership,[34] and even organize itself as if it were a partnership.[35]

B. Contemporary Legacy

One might think that joint venture doctrine—though now essentially defunct—would have left a legacy of case law and analysis that grapples with the intrinsic fiduciary conflict. It has not.

Instead, the only legacy is a mild confusion over the legal distinction between joint venture and partnership. In practice, the difference is essentially zero. Partnership law generally applies to joint ventures.[36] The reasoning behind this typically revolves around a simple inference: joint ventures are, by legal definition, similar to partnerships; therefore, partnership law should apply.[37] A related line of reasoning is that partnership law applies to joint ventures, but only “by analogy.”[38] The effect of this reasoning is that partnership law is usually applied to joint venture, but in a piecemeal fashion. When confronted with an issue that is settled in partnership law but has never been applied to a joint venture, a court will declare the question a matter of “first impression,” acknowledge the joint venture relation, state the “general rule” that partnership law applies, and finally conclude that partnership law governs.[39]

A few states admit idiosyncratic differences between partnership and joint venture law. The two most important concern termination procedures and voting rights. Partnerships are “terminable at will” by default.[40] Illinois, however, makes an exception for joint ventures: by default, joint ventures are not terminable until the purpose of the venture is achieved.[41] On voting, some states have different default ownership rights in joint venture versus partnership, and this can generate different voting procedures. In partnership, the default for all jurisdictions is that real property is owned by the partnership entity or by the partners as tenants in partnership.[42] However, Michigan makes an exception for joint ventures: the default is that co-venturers own real property as tenants in common.[43] The practical effect of this exception is that, in Michigan, partnership defaults concerning transfer of property are flipped for joint ventures: while tenants in partnership can transfer the entire, co-owned estate without a unanimous vote,[44] tenants in common must have a unanimous vote.[45] These two exceptions on default termination and voting rights, however, are idiosyncratic to particular states and have no effect on most cases.[46] Further, at least in some instances, courts arguably did not intend to create these exceptions.[47]

Though most jurisdictions seem to admit no difference between partnerships and joint venture law, only Texas and Maryland have expressly abolished the legal distinction by statute.[48] Thus, notwithstanding a few peculiarities (not to mention significant confusion in the case law) the law is easily summarized: in Texas and Maryland, joint venture and partnership are legally equivalent; in all other states, case law has approximately equated the two.

Since the law of corporate partnerships very quickly transitioned from outright prohibition to total contractual freedom, it is not surprising that there is no case law analyzing the intrinsic fiduciary conflict. The conflict simply did not spend enough time in the courts to evolve into a coherent doctrine.

This absence of doctrine was not inevitable. Indeed, many of today’s corporate doctrines evolved out of business activities that were previously prohibited. To give one example, consider the old common law rule against interested transactions. The rule was that any deal between the corporation and one of its agents was automatically voidable by the corporation.[49] Like the rule against partnerships, the rule against interested transactions was also overruled by statute.[50] Yet unlike the rule against partnerships, the rule against interested transactions eventually transitioned into a coherent doctrine. This was because the law did not relinquish control over interested transactions. Delaware, for example, only overruled the automatic voidability of interested transactions; its statute and case law replaced this with the threat of voidability—that is, a set of judicial standards to evaluate such deals.[51] By contrast, corporate law simply relinquished control over corporate partnerships; they were unconditionally enabled. Because of this, there were no cases, and so it is not surprising that there emerged no doctrine through which courts could grapple with the loyalty conflicts inherent in joint ventures.

The modern response to this conflict is thus not found in statute or case law, but in contract. In what follows, I lay out a study of such contracts. The goal is to understand how modern corporate joint ventures deal with the intrinsic fiduciary conflict. I will argue that a combination of a CNC and a separate joint venture entity form the key contractual solution.

II. Private Parties’ Response

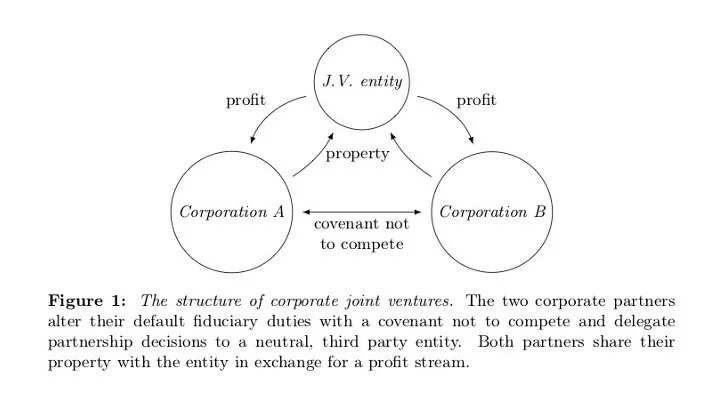

This Section presents a theory of how corporations respond to the intrinsic fiduciary conflict of joint venture. At the heart of this response lie two legal devices: (1) a CNC and (2) a separate joint venture entity. I argue that these devices work together to resolve the fiduciary conflict. The parties alter the default loyalty duties with the CNC while simultaneously sidestepping potential conflicts by operating their venture through a separate entity.[52] Figure 1 diagrams this structure.

This theory thus offers a new explanation behind CNCs: in corporate joint ventures, CNCs are the key mechanism for establishing coherent fiduciary duties. The theory also presents a novel use for entities: entities are often thought to create conflicts because they introduce the principal-agent problem, but I argue that in joint ventures they counterintuitively prevent conflicts because they enable partners to delegate conflicted decisions.

The main exposition will proceed with a case study from the aerospace industry. It should be kept in mind, however, that we observe this basic structure in corporate joint ventures across all industries.[53]

A. Case Study

In 2005, The Boeing Company and Lockheed Martin established a joint venture.[54] Their agreement formed a new, multi-billion-dollar company, United Launch Alliance (ULA), a Delaware LLC owned in equal shares by its two members.[55] The business of ULA is to launch satellites into orbit for the US government. Most of these services are provided to the US Air Force and NASA.

The ULA venture was the result of an Air Force program that began in 1994.[56] The program increased funding for the procurement of rocket systems from private companies. It ultimately led to the development of two competing rocket systems, one by Boeing (the “Atlas” system) and the other by Lockheed (the “Delta” system).[57] For many years, Boeing and Lockheed separately designed and manufactured their two systems. In the course of their competition, the US government awarded both companies several contracts throughout the 1990s and early 2000s.

The competition between these two firms was not only fierce, but at times illegal. Early in the Air Force procurement process, a Boeing executive solicited a Lockheed engineer to work at Boeing.[58] The Lockheed engineer brought thousands of pages of confidential documents to Boeing.[59] These documents exposed Lockheed’s plans for contract bidding as well as Lockheed’s new proposals to the Air Force.[60] In 2003, the Justice Department charged the executive and the engineer with conspiracy to steal Lockheed trade secrets.[61] The United States and Lockheed also filed separate civil actions against Boeing.[62] As a result, Boeing was fined, temporarily banned from providing launch services to the US government, and stripped of several of its existing contracts.

This was a low point in trust between the two firms, yet out of this mess came the ULA joint venture.[63] The details are unclear (and confidential), but much of the impetus behind ULA seems to have come from the Air Force. For national security reasons, it wanted to keep both Boeing and Lockheed rocket systems operational. To accomplish this, the Air Force encouraged a joint venture between the two firms. It expected (or hoped) that this would not only ensure their survival, but also result in higher quality launches.

Boeing and Lockheed, despite their pending suits and counter-suits, were probably happy to oblige since the venture would create a monopoly on launch services to the US government. The Federal Trade Commission noted this anticompetitive effect in its review of the proposed venture, but nevertheless approved the venture because of the Air Force’s concerns about national security.[64] Boeing and Lockheed settled their civil claims,[65] and—out of this dramatic conflict—their venture was born. They may have been rivals, and cheating rivals at that, but as partners they now owed each other a duty “of the finest loyalty.”[66]

B. Covenants Not to Compete (CNCs)

A covenant not to compete (CNC) is a contractual provision through which one party commits not to compete with another in a specified market. The next four subsections will (1) describe the CNC in the Boeing-Lockheed venture, (2) offer a new rationale for the role of CNCs, namely, to design coherent fiduciary duties in corporate joint ventures, (3) compare this new rationale with two traditional rationales for CNCs, and finally (4) argue that the new rationale I offer (designing fiduciary duties) is the fundamental purpose of a CNC in the context of a corporate joint venture.

1. CNCs in Action

The ULA venture included two types of CNCs. The first was a “non-solicitation agreement,” which covered promises over labor market demand and the movement of employees.[67] The second part of the CNC, the “non-competition agreement,” covered promises over product market supply. Together, these clauses ran about eight pages and constituted the most intricate—and confusing—sections of the 120-page ULA joint venture agreement.[68] To summarize the covenant not to compete, I will break it down into several parts.

First, Boeing and Lockheed defined their joint market as launch services for which: (1) the customer was the US government, (2) payloads were between 2–70 metric tons, and (3) payloads were delivered into low Earth orbit, which is between 160–2,000 kilometers above sea level. Boeing and Lockheed next agreed to refrain from two types of competition in this joint market: (1) for five years, neither would separately engage in the R&D of related products, and (2) for seven-and-a-half years, neither would separately engage in the manufacture or provision of related products.

Having cast a broad net, the non-competition agreement then made several exceptions. These included carve-outs relating to Boeing and Lockheed’s preexisting joint ventures,[69] carve-outs for “ordinary course” activities (twelve in total), and a severability clause—a kind of judicial carve-out that essentially asks the judge to make only the minimum modification necessary to cure an unenforceable CNC.

Finally, the non-solicitation agreement forbade all parties—Boeing, Lockheed, and the joint venture LLC—from actively soliciting certain of each other’s employees for two years. Although this affected the employment prospects of some top executives among Boeing, Lockheed, and the LLC, it had no effect on their ability to seek work outside of these three firms. Further, it was not an outright prohibition that would prevent, for example, a Boeing employee from changing jobs to Lockheed. Instead, it was merely a restriction on the procedure by which such a switch could occur: the partner corporation and the joint venture entity could not directly approach the employee. Given Boeing and Lockheed’s competitive history, particularly the instance of espionage between Boeing and Lockheed executives,[70] such a restriction seems prudent, if not necessary, to prevent each side from stealing the other’s trade secrets. The non-solicitation agreement included some exceptions based on both the rank and status of the employee (which were confidential).

2. A New Rationale for CNCs: Altering Fiduciary Duties

Why would a joint venture agreement adopt a CNC? Traditional law and economic theory have promoted two rationales based on the holdup and antitrust problems (which I summarize in the next section). Here, however, I offer a novel explanation for the primary function of a CNC in a corporate joint venture: corporations adopt them to alter fiduciary duties. CNCs are thus a key mechanism behind how corporations respond to the intrinsic fiduciary conflict of joint venture.

Without a CNC, Boeing would have had a duty to pursue partnership business opportunities for the benefit of both Boeing and Lockheed. But a Boeing agent could have easily become conflicted: what if, for example, the agent had to buy an input for the joint venture—and this input could only be purchased from one of the two partners?

The CNC solved this problem by prohibiting Boeing and Lockheed agents from even making this decision and instead delegating the decision to the independent agents of the joint venture LLC. Boeing still owed a partnership duty of loyalty to Lockheed. Under the CNC, however, it was satisfied by simply abstaining from action. Agents of Boeing did not have to compromise their corporate law duties by affirmatively acting in Lockheed’s interest.

To get a sense of how this works in practice, consider the intellectual property arrangement in the Boeing-Lockheed venture, where the intrinsic fiduciary conflict applied in full force. Boeing and Lockheed extended to ULA a free license over all their rocket-related intellectual property (discussed in more detail below). But this intellectual property could also be applied to purposes well outside the scope of ULA’s operations. For this reason, the Boeing-Lockheed licensing agreement included one significant exception: each firm retained the right to separately and independently exploit the same intellectual property in the ordinary course of its own business.[71] Because of this exception, Boeing and Lockheed could, and indeed do, continue to separately market their launch systems (the Boeing “Delta” and Lockheed “Atlas”) to commercial markets. The co-venturers are thus loyal partners with respect to technologies in one market, but aggressive competitors over the very same technologies in another. How is this possible? The answer is the CNC.

A CNC enables this competitor-partner dichotomy by regulating the duty of loyalty. To see this, first imagine a world without CNCs. In this case, the default duty of loyalty would govern. The default duty is a legal standard. It requires that each corporate partner “refrain from competing with the partnership in the conduct of the partnership business.”[72] This standard is used to determine which opportunities belong to the venture and which opportunities can be lawfully appropriated by either party. But like any standard, the boundaries are unclear. Judges, co-venturers, and even agents of the joint venture entity could hold reasonable but conflicting positions on what precisely constitutes “the partnership business” and whether any given opportunity lies strictly inside or outside of it.

CNCs organize the venture’s opportunities by swapping the default loyalty standard for a bright-line loyalty rule. The result is that co-venturers can more readily distinguish partnership opportunities from those which are “fair game” for either co-venturer to seize. For any given opportunity, both sides can more confidently don the “partners hat” or the “competitors hat.”

Though CNCs draw clear lines, they do not draw perfectly clear lines—nor should they. A CNC generally replaces fiduciary standards with fiduciary rules, and indeed some of the CNC carve-outs provide very clear lines. For example, Boeing and Lockheed were permitted to own exactly 10 percent or less of a competing business.[73] But both the CNC and the licensing provisions also expressly incorporated standards that were less clearly defined. For example, Boeing and Lockheed were permitted to separately engage in the R&D and manufacture of reuseable launch vehicles, as opposed to expendable launch vehicles, which was the defined business of the ULA venture. A reusable vehicle is one that is recovered after launch (such as the Space Shuttle), whereas an expendable vehicle is discarded after launch (usually by disintegrating on reentry). These may seem to be distinct concepts, but the line between them is not exactly bright. It could be analogized to the line between NASA’s Space Shuttle and Apollo programs. The former used reusable vehicles while the latter used expendable vehicles. The line between these programs may separate distinct projects and goals, but it does not separate distinct boundaries in intellectual property.

CNCs do not strive for the greatest clarity because certainty does not come for free. Requiring certainty means that co-venturers can only collaborate in markets that can be perfectly delineated. These markets do not necessarily coincide with the markets for which there are gains from collaboration. A more rule-like CNC discourages spontaneous collaboration outside the original scope of the joint venture, collaboration that could in turn lead to innovation that neither would have achieved separately. At the extreme, a “perfectly” delineated CNC would perfectly discourage such collaboration because the scope of the duty of loyalty is completely determined ex ante. Contrast this with a fiduciary standard. A fiduciary standard strongly encourages spontaneous collaboration because the scope of the duty is completely determined ex post: the scope is “the business of the partnership,” which, if left unspecified, is simply wherever the partners’ collaborations take them. Since technologies are often applied well beyond their original intention, a “perfect” CNC could prove counterproductive.

In summary, CNCs replace the loyalty standard with a level of clarity that balances the rule–standard tradeoff. In so doing, they mitigate the intrinsic fiduciary conflict by organizing joint venture opportunities.

3. Two Traditional Rationales for CNCs

Here I briefly outline two traditional rationales for CNCs based on the holdup and antitrust problems. The holdup problem arises where collaboration requires one or both sides to make relationship-specific investments.[74] The problem with such investments is that they are costly to redeploy outside the relationship. Having sunk a relationship-specific investment, the cost of backing out of the deal increases for the investing party. The counterparty is then incentivized to exploit the investing party’s vulnerability, to threaten to “hold up” the project and extract a larger share of the surplus. Ex ante, the threat of holdup inefficiently discourages relationship-specific investments.

A CNC mitigates the holdup problem by lowering the value of investments made outside the relationship. If a CNC is perfectly enforced, then investments made within the scope of the CNC but outside the relationship become worthless. Indeed, if CNCs are specifically enforced, then each party can enjoin the other from making such investments (or compel the other to divest if the investment is already made). The CNC thus provides indirect mutual assurance for relationship-specific investments: it does not prevent one party from threatening to walk away after the other has sunk a relationship-specific investment, but it does mitigate this holdup threat by limiting the breaching party’s outside options.

The antitrust rationale cuts two ways: co-venturers in similar markets prefer a broader CNC to capture a larger monopoly rent, while competition authorities prefer the opposite.[75] A joint venture’s CNC thus outlines a compromise between these two interests. For example, in the Boeing-Lockheed venture, the broad scope of the CNC was likely an advantage to Boeing and Lockheed because it provided more opportunities to monopolize the aerospace industry. But, in an effort to balance the monopolizing effect of the CNC, the Federal Trade Commission conditioned its approval for the venture on the implementation of certain pro-competitive policies, effectively altering the terms of the ULA CNC.[76]

4. The Fundamental Role of a CNC in Corporate Joint Ventures

In corporate joint ventures, the fundamental role of a CNC is to resolve the intrinsic fiduciary conflict; the holdup and antitrust motivations are of secondary importance. This is because the fiduciary role is logically prior. The holdup problem concerns opportunistic behavior in which one party purposely exploits the other’s vulnerability. The antitrust explanation is similarly purposeful: the partners are trying to grab as much market power as possible. Yet both explanations assume that these opportunistic and purposeful corporate agents actually know what their roles are.

The premise of this Article is that they do not. This is because corporate law and partnership law assign each agent two conflicting roles—or perhaps even three, if one considers the interests of the partnership entity as separate from the partners. Each agent must (1) advance the best interests of one’s own corporation (the corporate duty of loyalty), (2) advance the best interests of one’s partner corporation (the partnership duty of loyalty), and (3) advance the best interests of the joint venture entity (the “third” role, created by contract).

These fiduciary roles inherently conflict. Thus, this fiduciary conflict is logically prior to the antitrust or holdup problems: to exploit one’s own position, one must first know what it is. By forbidding each corporate partner from acting within the market defined by the CNC, the CNC “defines” the co-venturers roles by effectively eliminating all three. That is the innovation of the CNC. It carves out a negative space in which neither corporate partner may act. As explained below, the modern joint venture then fills this negative space with a separate entity whose role is to pursue the joint venture’s—and only the joint venture’s—interest.

C. Joint Venture Entities

Altering fiduciary duties with a CNC is only one half of the response to the intrinsic fiduciary conflict. We now arrive at the second, complementary half: the separate joint venture entity.

1. Using an Entity to Avoid Conflicts

Here I demonstrate a new function for entities: they are an innovative and deceptively simple response to the intrinsic fiduciary conflict. Perhaps the greatest challenge facing entities is that they create conflicts through agency, that is, through the separation of decision makers (agents) from beneficiaries (principals). The innovation of the joint venture entity is that corporations counterintuitively use a separate entity to avoid conflicts by delegating decisions for which the beneficiaries (i.e., the corporate partners) are conflicted. For example, consider again the one given above: suppose the joint venture had to buy an input from either Boeing or Lockheed. Boeing and Lockheed agents would both be conflicted; a third party must make this decision.

A joint venture entity thus serves the role of quarantining the venture’s opportunities. The Boeing-Lockheed venture created a new entity that is separate from both companies. The joint venture agreement itself was a contract among three parties: Boeing, Lockheed, and “a Delaware limited liability company to be formed.”[77] The “company to be formed” was United Launch Alliance, LLC.[78] ULA, the joint venture entity, acts as a buffer between the two co-venturers. Boeing and Lockheed may own the entity itself, but neither directly pursues the joint venture’s opportunities nor has the authority to make partnership decisions. Instead, all this is done through a third-party entity.

Critically, ULA has a separate set of agents who work only for ULA and not for either Boeing or Lockheed. As a matter of law, these managers owe a duty of loyalty to ULA itself, not to either co-venturer. Of course, there may be economic temptations that would bend the loyalties of ULA’s agents toward Boeing or Lockheed, especially because the managers themselves come from each: the LLC’s CEO is a former Lockheed manager, its COO is a former Boeing manager.[79] This assignment of in-house managers could create problems in enforcing the duty of loyalty. But before the LLC was established, the intrinsic fiduciary conflict created much more than a mere problem of enforcement: it was not even clear who owed what loyalty to whom. Further, the default duty of loyalty would have required Boeing agents to be loyal to Lockheed and vice versa. This would have been an impossible duty because Boeing and Lockheed are direct competitors. Creating a joint venture entity enables loyalties to remain “undivided” since no individual agent owes loyalty to more than one firm: Boeing agents are loyal to Boeing, Lockheed agents to Lockheed, and ULA agents to ULA. The enforcement problems may remain, but at least the duty itself is clear to both corporate partners.

The joint venture entity thus supplants the default structure of both loyalty and ownership over partnership opportunities. It replaces this with a structure in which partners retain ownership over the profits of the joint opportunities while the opportunities themselves remain out of reach. Instead of “joint custody” over the joint venture opportunities, there is “third-party guardianship.” Instead of having Solomon “split the baby,” Solomon himself—the neutral third—protects the baby.[80]

In addition to solving the intrinsic fiduciary conflict, entity creation also provides several additional conveniences. It limits the liability of both companies for the venture’s actions, serves as an accounting convenience to keep track of each party’s contributions and the venture’s operations, and clarifies the managerial chain of command. Operating the venture through an LLC (or other entity) also avoids the confusion in state law between joint venture and partnership. For example, some states maintain distinct (and sometimes confusing) procedures for terminating joint ventures and partnerships.[81] In contrast, Delaware provides clear statute and case law on when a co-venturer can petition the court to dissolve a joint venture corporation or joint venture LLC.[82] Creating an entity thus serves many roles that are separate from the intrinsic fiduciary conflict: economic, accounting, managerial, and legal. Conflict avoidance is yet another role, unique to joint ventures, that entities can play.

2. The Need to Collaborate Via an Entity

The joint venture entity also enables corporate competitors to collaborate. Direct collaboration would exacerbate the inherent fiduciary conflict. It would also mean disclosure of trade secrets and business practices to one’s competitor. Thus, instead of collaborating directly with each other, modern joint ventures collaborate indirectly through the joint venture entity.

In the Boeing-Lockheed venture, collaboration via an entity enabled the partners to share intellectual property without having to disclose it to their competitor. Boeing and Lockheed both granted ULA “a worldwide, perpetual, irrevocable, non-transferable, no-cost, royalty-free” license to their intellectual property portfolios relating to expendable launch vehicles (one-time-use rockets). The license was exclusive during the term of the CNC, meaning that ULA enjoyed both unrestricted and exclusive access to the rocket-related intellectual property of Boeing and Lockheed.[83] After the term expired, ULA’s access was still unrestricted but no longer exclusive.[84]

This is a formidable power on the part of ULA. Intellectual property is the core of an aerospace firm and many of its technologies are general. The same patents that go into the guidance and aerodynamics of rockets are also used to design airfoils and electrical systems on fighter jets or commercial airliners. Thus, though it is difficult to estimate precisely, the value of ULA’s access to intellectual property likely exceeded the (transferable) value of ULA itself.

This power created both uncertainty and vulnerability. The uncertainty was that Boeing and Lockheed’s relative contribution could not be easily quantified ex ante. Even ex post, it may not have been clear which side contributed more. A “pay per use” accounting scheme for patents (i.e., a price mechanism) would have mitigated this. Instead, the ULA joint venture agreement simply stated that Boeing and Lockheed would share their intellectual property with the LLC, free of charge. ULA’s access also left Boeing and Lockheed vulnerable. Instead of piecemeal assignment or tailored access to individual technologies, ULA was given keys to both kingdoms—with the sole restriction that it use the keys “within the scope of the purpose of [the venture].”[85]

This vulnerability was the very problem that the Massachusetts court cited in 1858, when it prohibited the corporate partnership in Whittenton Mills.[86] The problem was that one partner had “too much” access—and therefore control—over the other. The further problem was that such control was lawful within the realm of partnership law. To the court, this presented not just a fiduciary conflict, but a contradiction. As discussed above, the original solution seemed like the only one: prohibition.[87]

If it were the case that Boeing and Lockheed were general partners and granted each other unrestricted access to their intellectual property, they would be in a situation akin to the partners in Whittenton Mills. Each corporate partner would have too much access and control over the other’s operations. Their vulnerability would be protected only by a threat of mutually assured destruction. But Boeing and Lockheed did not grant each other such access. They granted it to the joint venture entity, whose independence is checked by the fact that it exists only by the grace of the co-venturers. Instead of mutual access, there is third-party access. Instead of mutual control over all the partners’ business, there is third-party control over only the joint business.

Co-venturer shareholders in a joint venture firm thus differ from shareholders in a typical firm in several respects. First, shareholders of a corporate joint venture firm can appropriate the firm’s business opportunities. Indeed, the shareholders of ULA (Boeing and Lockheed) previously competed in the precise market in which ULA operated. Thus, one of the roles of the separate ULA entity was to protect the joint venture’s assets from its own shareholders. By contrast, the typical firm does not need to protect its assets from its own (small) shareholders. There is virtually no risk that a small shareholder of a typical firm will appropriate one of the firm’s opportunities. A small shareholder is often not able to even evaluate the business opportunities, let alone appropriate them.

The second difference is that co-venturer shareholders are integrated with the joint venture firm, that is, they coordinate with the joint venture firm without relying on a price mechanism. In the Boeing-Lockheed venture, the integration came in the form of “cost-free” access to the co-venturers’ intellectual property. This access was not mutually granted to each co-venturer, but instead granted to the joint venture firm. The integration was thus not between the co-venturers themselves, but between the co-venturers and their joint venture entity. By contrast, the typical shareholder is not integrated with the firm; the typical shareholder does not share assets with the firm.

Finally, there is no intrinsic fiduciary conflict among shareholders of a typical firm. The firm’s agents owe loyalty only to the corporation, while the shareholders owe no loyalties at all.[88] Put another way, shareholders of traditional dispersed corporations are not partners.

III. Enforcement Problems and Proposed Solution

This Section discusses differences across states in their willingness to enforce CNCs, as well as their willingness to let co-venturers alter fiduciary duties. It then offers a policy recommendation: an internal affairs doctrine for corporate joint ventures. Under this rule, parties would be allowed to choose the law that governs their joint venture and courts would enforce that choice.

A. Enforcement Problems

1. Are CNCs Enforceable?

States vary considerably in their willingness to enforce CNCs. Here I consider two illustrative jurisdictions that delimit the ends of this spectrum of enforceability: Delaware and California.

Delaware embraces CNCs as the source of a corporate joint venture’s fiduciary duties. In Universal Studios, Inc. v. Viacom, Inc.,[89] the Delaware Chancery Court considered a joint venture that was structurally similar to the Boeing-Lockheed deal. Two corporations, Universal and Paramount, formed a partnership called the USA Network, which soon became a successful cable network. The core provision of their deal was a CNC that prevented the partners from operating competing cable networks. There were some exceptions for their preexisting businesses, though these exceptions may not have been necessary because neither had competing cable networks. Some years later, Paramount was acquired by Viacom. Viacom had several preexisting cable network subsidiaries (including MTV and VH1). Universal then sued Viacom, claiming that by continuing to hold on to these networks, it violated the CNC.

The court made several holdings, all of which favored the interpretation of the CNC as an enforceable source of fiduciary duties. Universal argued that Viacom’s acquisition tortiously interfered with the USA Network partnership agreement. The court rejected the claim, writing that “[a] more appropriate analysis of Viacom Inc.’s actions must be within a discussion of the parties’ fiduciary duties.”[90] It then held that the CNC was the exclusive source of these duties:

The parties . . . intended to define the participants’ duty of loyalty to each other and to the Venture partnership within the non-compete or covenant not to compete clause. As such, I need not discuss the issue of any independent breach of common law fiduciary duty. All of the parties’ respective contentions concerning the scope of the duty, the existence of a breach of duty, the effect of the breach, the nature of the harm suffered by the USA Networks, and who bears responsibility as a result, can and should be discussed within the framework crafted by the parties themselves—the non-compete clause and associated provisions of the contractual relationship.[91]

The court ultimately found that Viacom had breached its duty of loyalty to Universal.

The court thus endorsed the idea that corporate partners define their fiduciary duties through a CNC. The case also demonstrates that Delaware is willing to enforce a CNC in the context of corporate joint ventures.

California, in great contrast to Delaware, takes a less permissive approach to CNCs. CNCs are notoriously difficult, if not impossible, to enforce in California. Section 16600 of the California Business and Professions Code imposes a blanket prohibition that voids any “contract by which anyone is restrained from engaging in a lawful profession, trade, or business of any kind.”[92]

This prohibition applies even in the context of an ongoing joint venture. In Kelton v. Stravinski,[93] two natural persons, along with their associated corporations, formed a series of partnerships to develop warehouses. Their first agreement included a CNC: each party agreed not to pursue future warehouse projects without the other. Kelton used this agreement to claim an interest in projects that Stravinski had pursued outside the partnership. The trial court rejected Kelton’s claim and held that the covenant was unenforceable as a matter of law under section 16600.[94] The appeals court affirmed, holding that “[i]n the partnership context, an ongoing business relationship does not validate the covenant.”[95] Further, the appeals court separately held that Kelton could not recover under a duty of loyalty claim because subsequent amendments to the agreement had limited the scope of partnership to its existing projects.[96] The court did not reach the question of whether a partner could enforce a CNC by claiming that it defines the venture’s duty of loyalty. Thus, it is not clear whether and to what extent joint venture agreements with CNCs are enforceable in California.[97]

2. Are Fiduciary Duties Alterable?

The default and mandatory fiduciary boundaries of joint ventures are governed by partnership law.[98] Here I again consider California and Delaware, which delimit the spectrum of the extent to which states permit alteration of these duties. In previous work, I have shown that these jurisdictions are among the most commonly chosen by sophisticated parties.[99]

California limits co-venturers’ power to tailor fiduciary duties. Like most states, California adopted the Revised Uniform Partnership Act’s (RUPA) position on altering fiduciary duties.[100] California law provides that a partnership agreement “may not . . . eliminate the duty of loyalty,” but that it may exempt specific behavior by describing it in detail.[101] However, exempted behavior is still subject to judicial review.[102]

In the Boeing-Lockheed case, if California law had governed the CNC, it is unlikely that Boeing and Lockheed would have been able to enforce their alteration of fiduciary duties, especially if a dispute had arisen over one of the agreement’s enumerated exceptions for certain “ordinary course” activities. This is because a partnership opportunity must be specifically described in the contract before it may be lawfully appropriated. It should come as no surprise then, that the Boeing-Lockheed deal did not select California law (or any other RUPA state), but instead chose Delaware.

Delaware enables partners to opt out of the duty of loyalty. Delaware adopted RUPA but changed the rule for altering fiduciary duties. The Delaware statute replaces the elaborate altering provisions of RUPA with a simple statement that partnership agreements “may not . . . [e]liminate the implied contractual covenant of good faith and fair dealing.”[103] Delaware law explicitly states that this, along with other changes to RUPA, were made to promote freedom of contract.[104]

A partner that contracts out of loyalty in Delaware can lawfully appropriate a partnership opportunity without disclosing it ex ante or accounting for its benefits ex post.[105] This is not possible under RUPA.[106] However, the duty to disclose partnership opportunities should not be conflated with the duty to disclose information about the partnership itself (i.e., its books and records). This duty is mandatory in all states.[107]

B. Policy Recommendation: An Internal Affairs Doctrine for Corporate Joint Ventures

The variation across state law in parties’ ability to enforce CNCs introduces legal uncertainty in corporate joint ventures. The uncertainty is over the extent to which co-venturers can alter and enforce fiduciary duties. The central claim of this Article is that the baseline fiduciary duties of corporate joint ventures— those imposed by corporate and partnership law—inherently conflict. Thus, corporate partners must design their own, coherent set of fiduciary duties. For this reason, I recommend the following policy: an internal affairs doctrine for corporate joint ventures.

Before discussing this policy, first consider the logical alternative: changing partnership law to accommodate corporate joint ventures. This would be a mistake for several reasons. Reforming partnership law would require colossal effort and might introduce more uncertainties. Partnership law was not designed with corporations in mind.[108] The partnership as a business association was designed for natural persons, and as the default business association, it is an especially powerful tool for promoting fair dealing among laypersons who go into business without choosing a business form. Partnership statutes and case law are also slow to evolve. New York, for example, still uses the original Uniform Partnership Act of 1914.

By contrast, an internal affairs doctrine would be straightforward to implement. It would only require a court to honor the choice of law made by the parties to the joint venture.[109] Its operation would be analogous to the internal affairs doctrine in corporate law. And though there are notable exceptions, even California courts are relatively willing to honor the choice of law in corporate charters.[110] Crucially, courts would uphold corporate partners’ choice of law even if it requires them to enforce a CNC that would otherwise be unenforceable under their home law.

Courts should be more willing to enforce CNCs in joint ventures (especially ones that have passed federal antitrust scrutiny) because the usual policy arguments against such covenants do not apply with the same force in the context of joint ventures. In a seminal article, Ronald Gilson analyzed CNCs in employment agreements.[111] Such agreements forbid an employee from working for a competitor firm, typically for a few years after leaving their current firm. Gilson’s study highlights the social tradeoff that such agreements present: enforcing them encourages innovation by protecting IP and preventing employees from disclosing trade secrets, but not enforcing them also promotes innovation through labor market mobility and information spillovers.[112] Gilson then persuasively argues that the non-enforceability of such agreements in California may have been a blessing for the development of Silicon Valley, where information spillovers were the key to innovation.

The calculus changes, however, in the context of corporate joint ventures. CNCs in joint ventures are typically not blanket prohibitions that prevent employees from working at unrelated competitor firms. Rather, they prevent the corporate partners from opportunistically poaching each other’s employees and their venture’s business opportunities. CNCs are the crucial mechanism for establishing a coherent set of fiduciary duties vis-a-vis the corporate partners.

Courts should not make the mistake of thinking that enforcing a joint venture’s CNC necessarily promotes competition. From afar, Boeing, Lockheed, and the joint venture LLC might look like three distinct firms that would compete were it not for the CNC. Indeed, each company has its own separate legal personality and separate loyal agents. However, Boeing and Lockheed are both competitors and collaborators. Both companies are integrated with the joint venture LLC; they share their intellectual property with it. There might be a competitive benefit to voiding their agreement—perhaps a marginal Boeing agent would efficiently switch jobs to Lockheed. But Boeing agents are always free to switch to firms other than Lockheed or the joint venture LLC.

Furthermore, any competitive benefit is potentially swamped by the loss of collaborative innovation: without a CNC, there is no coherent fiduciary relationship; the partnership would not exist. This is not to say that any given joint venture’s CNC is socially beneficial, or even that the Boeing-Lockheed CNC is beneficial. Indeed, CNCs that generally prevent rank-and-file employees (as opposed to top executives) from switching firms are socially undesirable, unnecessary, and unfair. The point here is not to advance a position on the precise boundaries of an optimal CNC enforcement policy. Instead, the point here is that the policy calculus behind enforcing CNCs is fundamentally different in the context of a joint venture. The law ought take this difference seriously by adopting an internal affairs doctrine. Such a doctrine would allow co-venturer corporations to choose the law that governs intra-joint venture disputes.

IV. Joint Venture Networks

This Section empirically demonstrates the existence of joint venture networks. By “joint venture network,” I mean the situation in which three or more firms simultaneously engage in separate joint ventures with each other. I argue that these networks exacerbate the intrinsic fiduciary conflict. I also argue that these networks require us to update the theory of the firm.

A. Existence and Scale

Figure 2 gives a hint of the enormity of the aerospace joint venture network. It graphs the network for Boeing, Lockheed, and BAE Systems.[113] I found thirty joint ventures that involve at least one of these three companies.

Yet Figure 2 significantly underestimates the scale of the aerospace network—even among these three firms. The biggest reason is that it only includes ventures that directly involve one of these three. “Partners of partners” are not depicted. The scale is further underestimated because I personally gathered the sample. In my attempts to cobble together annual reports, industry reports, and news articles, I almost surely missed some joint ventures.[114]

Figure 2 also understates the complexity of the true network structure. Lockheed and BAE, for example, have two joint ventures together. One of them involves Rafael Advanced Defense Systems (an Israeli firm), and the other involves Airbus (a European conglomerate) and Finmeccanica (Italy). A single joint venture can also give rise to several entities, each with its own distinct purpose, yet part of the larger partnership. Perhaps most confusing of all, joint venture entities themselves form joint ventures.[115] Figure 2 compresses these complexities into a single link between the parent companies. The full picture is thus much grander in scale and complexity.

There are several structural reasons for the proliferation of joint ventures in aerospace. These reasons run the gamut from economic to political motives. As for economic rationale, aerospace products must integrate complex systems—airframes, engines, weapons, communications—into a single product. One way to conceptualize this industry is that each firm specializes in a few systems and any given product is either sourced from several firms or developed through a joint venture. Relatedly, joint ventures are also key to maintenance of existing products. For example, in the commercial airline industry, ventures often form among the airframe manufacturer, the airline company, and local airport authorities.

The political rationale is specific to aerospace. International ventures sometimes form as a response to the military procurement bureaucracy. The bureaucracy is a myriad of regulatory and political hurdles for any supplier, but it is especially cumbersome for the foreign supplier.[116] International ventures are sometimes created to “domestically” source technologies, either because direct foreign sourcing is prohibited or because the bureaucracy is too treacherous for the foreign firm to navigate alone.

International joint ventures can also arise out of a desire for political cooperation. Many of the North Atlantic Treaty Organization (NATO)’s suppliers, for example, are joint ventures among the large aerospace firms of member states.[117] It should be noted, however, that ventures form even in the face of domestic pressure not to trade with foreign governments.[118] International ventures thus form both because of and in spite of international political constraints.

B. Dynamic Networks

The aerospace joint venture network presents the intrinsic fiduciary conflict writ large. In the context of a single joint venture, the entity-CNC combination is, at the very least, an extremely convenient organizational device. In the context of an interconnected industry such as aerospace, this device becomes critical to sustaining the joint venture network.

Before their ULA venture, both Boeing and Lockheed were independently engaged in separate joint ventures with the same third firm, RSC Energia, a large state-owned aerospace company in Russia. Both joint ventures also provided launch services—and so they were seemingly competitors.[119] However, the Boeing-Lockheed CNC enabled both firms to maintain their respective positions because it was conditioned on (1) sales to the US government and (2) launch services to low Earth orbit. In contrast, their existing ventures were for sales to commercial customers and launches into medium and high Earth orbit.[120] This latter fact quite literally put their preexisting ventures thousands of miles beyond the scope of the ULA venture.[121] The agreement thus enabled both firms to continue their respective ventures with RSC Energia.[122]

Joint venture networks are thus dynamic. Figure 3 diagrams the joint venture network among Boeing, Lockheed, and RSC Energia before and after the ULA joint venture. The dashed links indicate changes to the network after ULA was formed.

CNCs take a larger role in the context of a dynamic joint venture network. A CNC delineates the loyalty boundary for a given dyad. This makes it easier for each co-venturer to then turn around and cooperate with another company, for those companies to in turn form partnerships with others, and so on. Even if a fuzzy loyalty standard were optimal for a given dyad in isolation, it probably would not be optimal for a given company in a network. This is because the costs of an uncertain loyalty standard are compounded over a network. Uncertainty over loyalties translates to uncertainty over ownership of corporate opportunities. This creates uncertainties in neighboring ventures, both realized and potential. If A and B form a venture with fuzzy boundaries, how can C plan a potential venture with either? Suppose C forms a venture with B; then what is D to make of the fuzzy boundary from A to B and B to C? CNCs, along with separate joint venture entities, mitigate the propagation of this negative externality—both across firms and within ventures for a given firm. Together, they clarify the loyalty duties and insulate the corporate partners from the source of potential conflicts—that is, from the partnership’s day-to-day activities.

C. Implications for the Theory of the Firm

The vastness of the aerospace network compels a simple question for the theory of the firm: where are the firm boundaries? Joint venture networks do not conform to a traditional theory of the firm. If A, B, C, and D are the 4 firms of an industry, and in the course of their competition they form and maintain all possible combinations of joint ventures (11 in total),[123] does that mean that there are 4 + 11 firms? Or still just 4? Or 1 mega-firm?

The industry may have begun as a set of disjoint firms. And even after all 11 joint ventures are created, firms A, B, C, and D—by themselves—would continue to form a partition of the industry. That is, they are disjoint firms that together account for all the industry’s activity. But A, B, C, and D would no longer be an exhaustive list of all firms. There are firms A, B, C, and D separately, but there are also joint venture firms {A, B}, {A, C}, {A, D}, and {A, B, C}, not to mention the potential “joint venture of joint venture” firms.[124]

The theory of the firm starts with the premise that firms are a coherent unit of observation, that they are distinct and separate from each other, and that transactions either occur strictly “within the firm” or “in the marketplace.” This applies to all flavors of the theory of the firm, whether premised on transaction costs, control, ownership, or contract.[125]

The existence of joint venture networks challenges this assumption. In the aerospace industry, the “foundational” firms such as Boeing and Lockheed overlap with each other through their much more populous joint venture firms. Since corporate partners are integrated with the joint venture entity but not with each other, the joint venture transaction occurs both between and within firms. Firms may be distinct entities, but they are not necessarily disjoint entities. The boundaries of the firm overlap with one another.

Conclusion

Corporate joint ventures, by combining the corporate and partnership business forms, create an intrinsic fiduciary conflict. The conflict is that corporate law imposes a duty of loyalty toward one’s own company, while partnership law imposes an opposite duty of loyalty toward one’s partner company. This Article examined how private parties and the law can and should respond to this conflict.

The Article made three contributions. First, it showed that there is a conflict within the fiduciary duties of corporate joint ventures. This conflict has not been previously recognized by the literature. The Article presented a theory of how modern corporations respond to this fiduciary conflict: (1) by altering the default loyalty duties through a CNC; and (2) by avoiding conflicts by operating the venture through a separate entity. This theory thus suggested a new role for CNCs: they are the lynchpin of fiduciary duties in corporate joint ventures. It also suggested a novel role for entities, which are often thought to create conflicts because they introduce the principal-agent problem; instead, I showed that joint ventures counterintuitively employ entities to avoid conflicts by delegating decisions for which the corporate partners are conflicted.

The second contribution concerned enforcement. Some jurisdictions restrict partners’ power to alter the default duties and enforce CNCs, while others enable partners to do both. This creates legal uncertainty for corporations looking to form joint ventures. The Article offered a policy recommendation to mitigate legal uncertainty: an internal affairs doctrine for corporate joint ventures. Under this rule, parties would be allowed to choose the law that governs their joint venture and courts would honor that choice.

The final contribution was to empirically demonstrate the existence of joint venture networks. These complex networks further compound fiduciary conflicts and require us to update the theory of the firm.

DOI: https://doi.org/10.15779/Z38G73740T.

Copyright © 2018 California Law Review, Inc. California Law Review, Inc. (CLR) is a California nonprofit corporation. CLR and the authors are solely responsible for the content of their publications.

Sarath Sanga, Northwestern University Pritzker School of Law. Email: sanga@northwestern.edu. I thank Eric Talley, Robert E. Scott, Kerem Sanga, Jeffrey Rachlinski, Gabriel Rauterberg, Roberta Romano, James Pfander, Justin McCrary, Kate Litvak, Jeffrey Gordon, Victor Goldberg, James Texas Dawson, Richard R.W. Brooks, Patrick Bolton, Bernard Black, and Ian Ayres for very helpful comments. This research was supported by the Northwestern University Pritzker School of Law Faculty Research Program.

- Alexander Pope, An Essay on Criticism pt. 2 (1709) (“A little Learning is a dang’rous Thing / Drink deep, or taste not the Pierian Spring . . . .”). ↑

- The Restatement (Third) of Agency section 1.01 provides: “Agency is the fiduciary relationship that arises when one person (a ‘principal’) manifests assent to another person (an ‘agent’) that the agent shall act on the principal’s behalf and subject to the principal’s control, and the agent manifests assent or otherwise consents so to act.” ↑

- See, e.g., Del. Gen. Corp. L. (DGCL) § 102(b)(7)(i) (2015); Revised Uniform Partnership Act (RUPA) § 404(b) (2017); Uniform Partnership Act (UPA) § 21 (1914). ↑

- RUPA § 404(b)(3). ↑

- Meinhard v. Salmon, 164 N.E. 545, 546 (N.Y. 1928). All jurisdictions have held that the default duties in partnership (undivided loyalty) also apply to joint ventures. See infra Part I.B. ↑

- Meinhard, 164 N.E. at 548. ↑

Examples of large joint ventures among such companies include Boeing and Lockheed (aerospace), AMD and Fujitsu (integrated circuits), MolsonCoors and SABMiller (beverages), Forest and Merck (pharmaceuticals), General Mills and Nestle (food and beverage), Goodyear and Sumitomo (tires), Hasbro and Lucasfilm (toys), Fossil and Seiko (watches), Deere and Hitachi (heavy industry and farm equipment), and E-Trade and Softbank (retail investment and telecom).

A large literature examines the structure and formation of corporate joint ventures. *See, e.g.*, Ronald J. Gilson, Charles F. Sabel & Robert E. Scott, *Contracting for Innovation: Vertical Disintegration and Interfirm Collaboration*, 109 Colum. L. Rev. 431 (2009) (studying enforcement of collaborative and long-term supply contracts); Gary Pisano, *The R&D Boundaries of the Firm: An Empirical Analysis*, 35 Admin. Sci. Q. 153 (1990) (on the decision between in-house versus external sources of research and development); Gary Pisano, *The Governance of Innovation: Vertical Integration and Collaborative Arrangements in the Biotechnology Industry*, 20 Res. Policy 237 (1991) (surveying governance structures of biotechnology ventures); Zenichi Shishido, *Conflicts of Interest and Fiduciary Duties in the Operation of a Joint Venture*, 39 Hastings L. J. 63 (1987) (describing varieties of fiduciary conflicts that could arise between co-venturer corporations). On the tension between competition and cooperation among corporate actors, see generally Adam M. Brandenburger & Barry J. Nalebuff, Co-opetition (1996). [↑](#footnote-ref-8)

On the law and economics of fiduciary duties, see Robert Cooter & Bradley J. Freedman, The Fiduciary Relationship: Its Economic Character and Legal Consequences, 66 N.Y.U. L. Rev. 1045 (1991) (on burdens of proof and appropriation of opportunities); Jeffrey N. Gordon, The Mandatory Structure of Corporate Law, 89 Colum. L. Rev. 1549 (1989) (on the nature and function of these duties as mandatory versus default); Jonathan R. Macey, An Economic Analysis of the Various Rationales for Making Shareholders the Exclusive Beneficiaries of Corporate Fiduciary Duties, 21 Stetson L. Rev. 23, 36–39 (1991). On the enforcement of covenants not to compete in executive employment contracts, see Sarath Sanga, Incomplete Contracts: An Empirical Approach, 34 J. L. Econ. & Org. (forthcoming 2018). For an analysis of the corporate opportunities doctrine from the perspective of contract theory, see Eric Talley, Turning Servile Opportunities to Gold: A Strategic Analysis of the Corporate Opportunities Doctrine, 108 Yale L. J. 277 (1998). On innovations in contract generally, see Kevin E. Davis, Contracts as Technology, 88 N.Y.U. L. Rev. 83 (2013).